Jacob Valenbreder

Jacob Valenbreder

·

Why Manual Claims Review Is Your Biggest Hidden Cost

Why Manual Claims Review Is Your Biggest Hidden Cost

It doesn't show up as a line item. But it's quietly consuming a larger share of your operating budget than almost anything else in your claims operation.

Ask any Head of Claims where their biggest cost sits and you'll hear the same answers: fraud losses, litigation, reinsurance. Manual review rarely makes the list. But strip back the loaded hourly rates, the rework loops, the SLA breach penalties, and the talent cost of keeping experienced adjusters doing repetitive triage, and a different picture emerges.

Manual claims review isn't just slow. It's a structural cost problem that compounds as volume grows, and most insurers are underestimating it by a significant margin. According to J.D. Power's 2024 Property Claims Satisfaction Study, average property claims cycle time has reached 23.9 days, over six days longer than in 2022. For travel insurers, the picture is even sharper: travel insurance claims increased 18% in 2024 compared to 2023 (Squaremouth), meaning that operational debt is growing faster than most operations are equipped to handle.

The Cost You're Not Measuring

Most claims operations measure cost-per-claim as a headline number. What that figure rarely captures is the fully loaded cost of the human steps involved in a manual review cycle. Research from Deloitte's Insurance Claims Transformation Report found that adjusters spend up to 40% of their time on administrative tasks rather than actual claims evaluation. For a function hired to exercise professional judgment, that ratio represents a significant structural inefficiency.

The specific costs that go unmeasured include:

Adjuster time spent on data entry, document retrieval, and coverage cross-referencing. None of these tasks require professional judgment, yet they dominate an adjuster's working day.

Rework cycles triggered by incomplete submissions, incorrect data, or system mismatches, with each loop adding days to handling time.

Escalation overhead when borderline cases get passed up the chain due to lack of a structured decision framework.

SLA breach costs, including both financial penalties and the reputational damage of slow claimant communication.

Opportunity cost: the complex, high-value cases that experienced adjusters never reach because their capacity is absorbed by volume work.

Add these together across a portfolio of thousands of claims per month, and the number stops being a rounding error.

Adjusters spend up to 40% of their time on administrative tasks rather than actual claims evaluation. For a function hired to exercise professional judgment, that ratio is the core of the problem [2].

Volume Is the Multiplier

The problem with manual review isn't just that it's expensive per claim. It's that the cost scales linearly with volume. Every additional claim demands a proportional increase in headcount, tooling, and management overhead, with no efficiency gain at higher throughput.

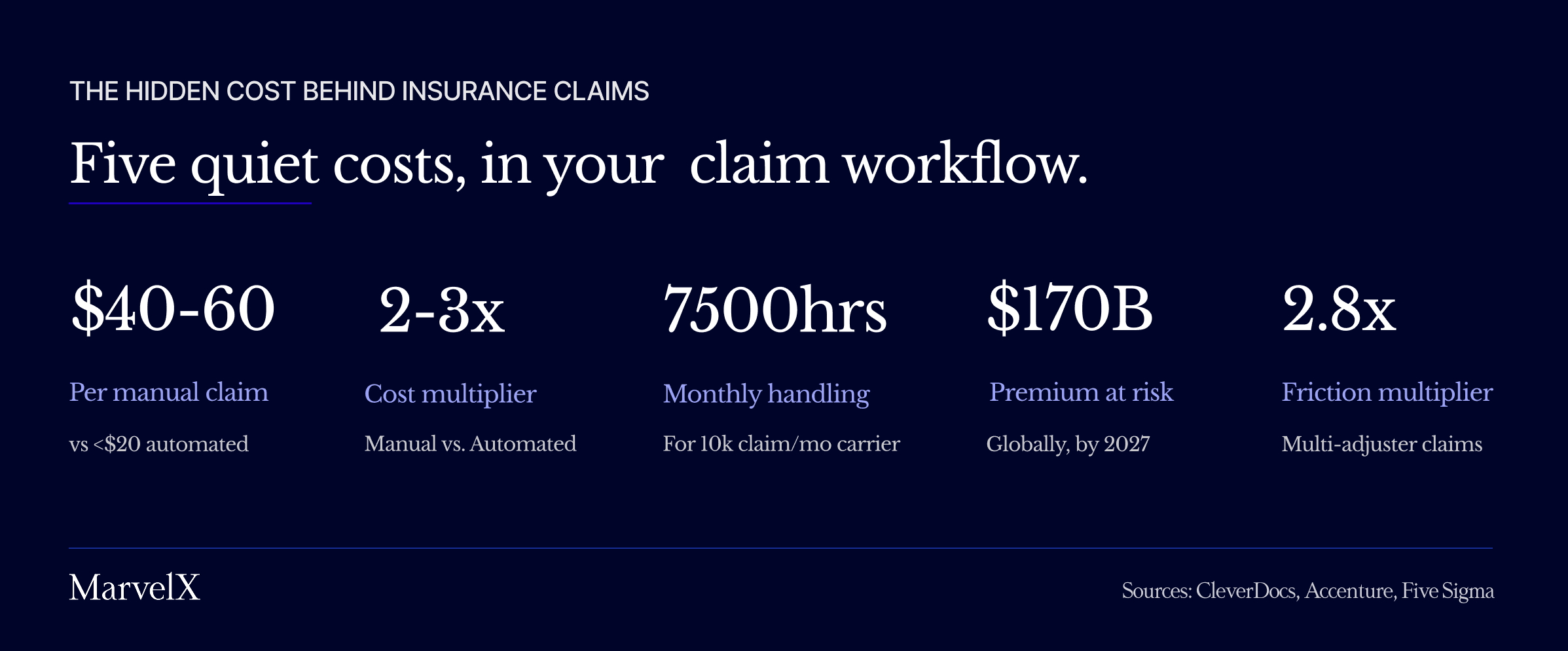

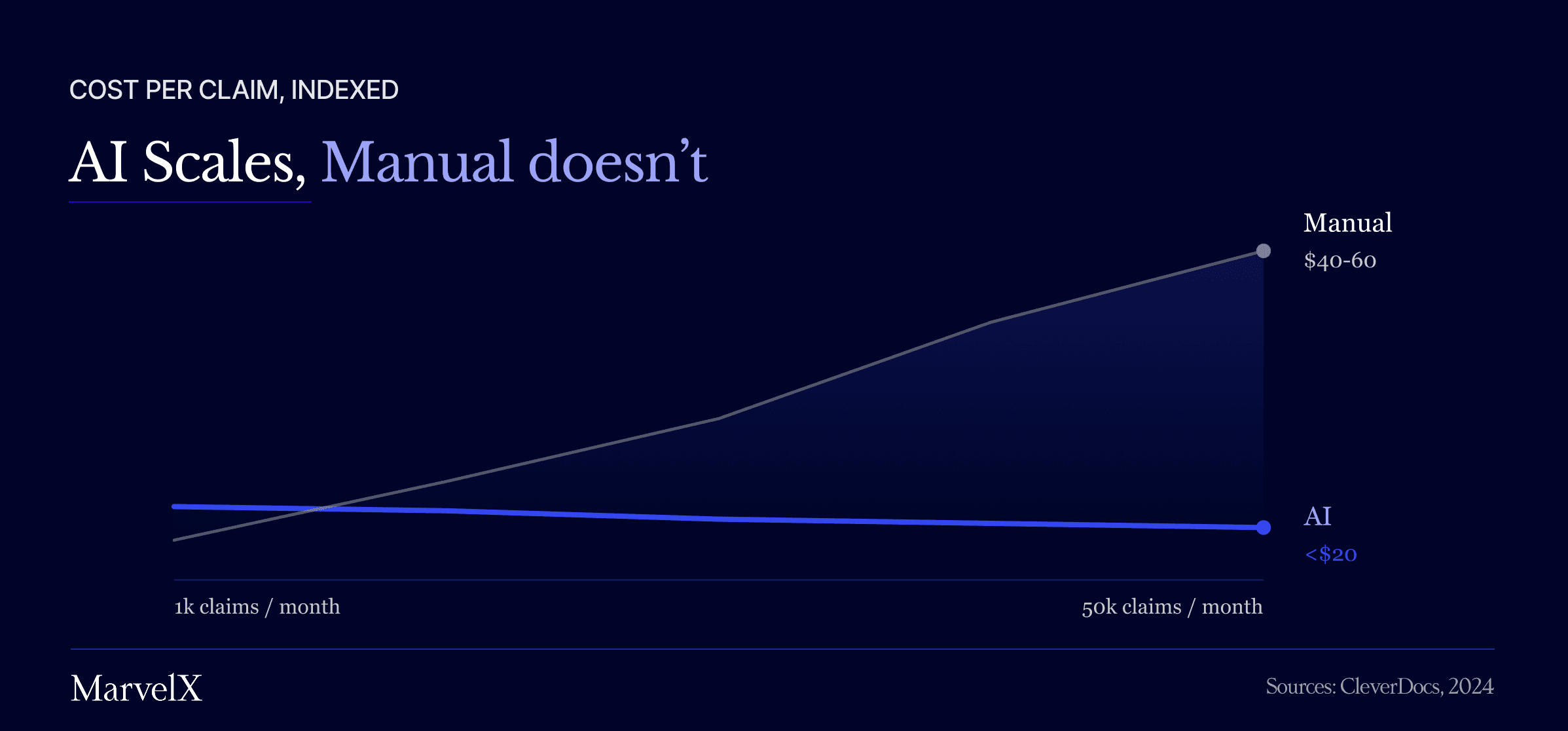

The data makes this concrete. Manual processing currently costs $40 to $60 per claim compared to under $20 for automated claims. That's a cost differential that becomes unsustainable at scale. For a mid-size carrier processing 10,000 claims per month, even a conservative estimate of 45 minutes of manual handling per claim amounts to roughly 7,500 person-hours monthly. At loaded labour cost, that's a seven-figure annual expense, before a single fraud case is caught or a single SLA breach occurs.

The travel insurance sector illustrates this acutely. With claims volumes up 18% in 2024 and average trip costs rising 25% year-on-year [6], the financial exposure per claim is growing at the same time as volume, compressing margins from both directions. Carriers relying on manual processing to handle this growth are effectively choosing to pay more per claim while handling more of them.

Critically, that cost doesn't decrease when claim complexity decreases. Straightforward, low-value claims consume roughly the same manual touchpoints as complex ones. The effort is in the process, not the case.

Where the Budget Is Actually Going

Across carriers, MGAs, and claims outsourcing providers, the manual review cost structure typically breaks down into three buckets.

1. Direct Labour: the visible cost

Adjuster salaries, team lead oversight, QA review layers, and the management overhead required to maintain throughput. This is the cost most CFOs see on a spreadsheet, but even here, utilisation data is rarely scrutinised. The percentage of adjuster time spent on truly judgment-intensive work is consistently lower than leadership assumes: industry data puts administrative tasks at up to 40% of working time, with the most experienced adjusters most constrained by this.

2. Process Friction: the cost no one owns

Rework loops, missing documentation requests, inconsistent coverage decisions across adjusters, and inter-system data handoffs. These costs are diffuse, never sitting in a single budget line, but compounding across every claim that touches more than one human. Five Sigma's analysis of thousands of real claims found that when a claim requires more than one adjuster, handling time nearly triples (2.75 to 2.85x average)[3]. For a claims operation where multi-adjuster claims are the norm on complex lines, this is not a marginal cost.

3. Downstream Risk: the cost you discover late

SLA penalties, regulatory breach exposure, fraud that slipped through inconsistent review, and claimant churn from poor communication. Accenture's research across 6,700+ policyholders in 25 countries found that poor claims experiences put up to $170 billion in global insurance premiums at risk by 2027 [5]. These costs often appear in different budget lines (legal, compliance, customer retention), making the root cause invisible in reporting.

A Clear Example: Travel Insurance

Travel insurance claims offer one of the sharpest illustrations of what the manual processing cost problem looks like in practice, and what becomes possible when it's removed.

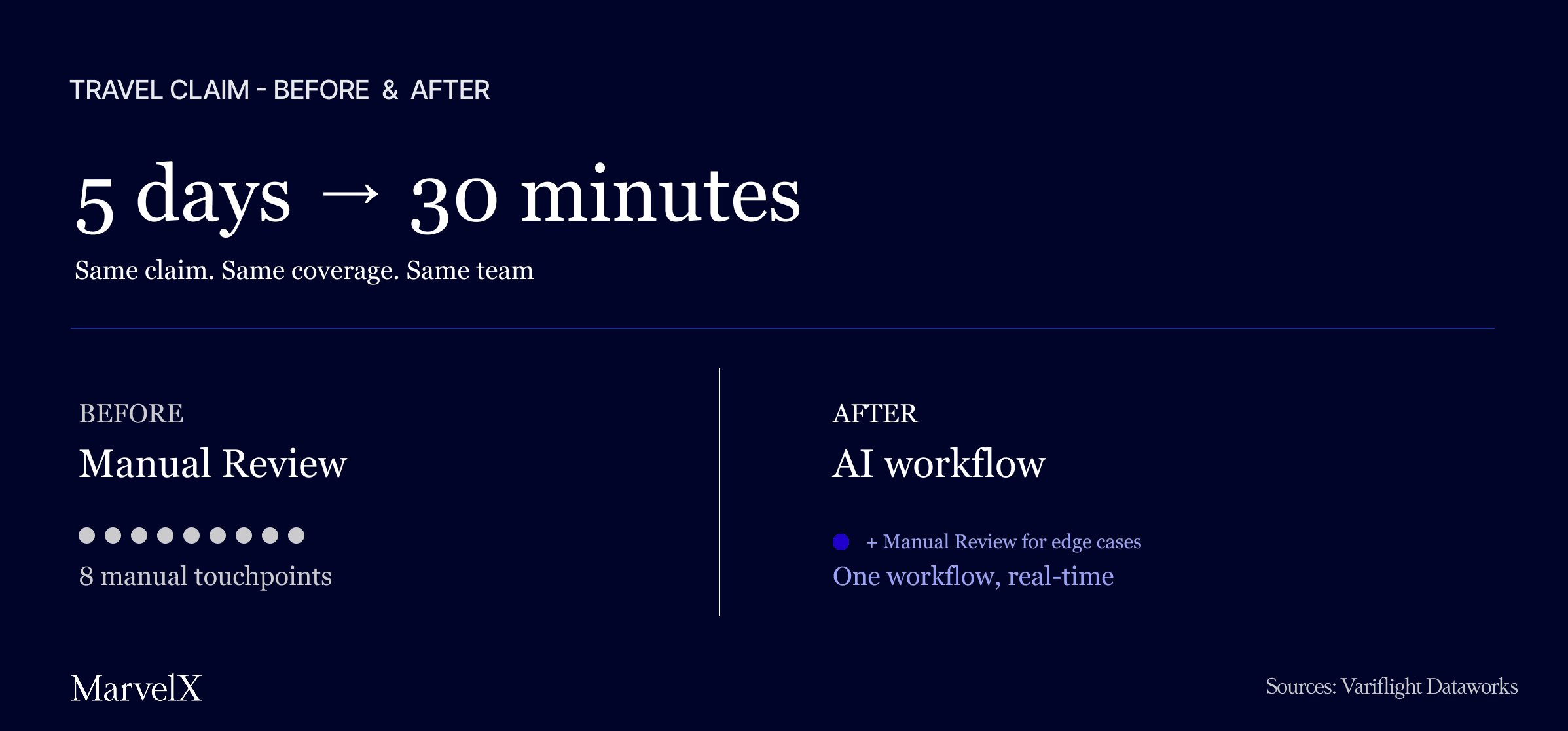

In 2025, an Asia-Pacific travel insurer integrated real-time flight status data into their claims workflow. The result: claim processing time for flight delay claims dropped from five days to under 30 minutes [7]. The same claims. The same coverage. The same adjuster team, now freed from a process that had been consuming their capacity on the most routine, predictable claims in their portfolio.

This isn't an edge case. Travel claims are structurally well-suited to illustrate the broader problem: they involve high volumes of straightforward, verifiable events (delays, cancellations, medical emergencies) that are currently processed through the same manual review channels as complex, high-judgment cases. The overhead is disproportionate to the decision complexity.

Research consistently bears this out. In travel insurance specifically, 60% of claimants cite slow settlement times as a major source of dissatisfaction. Across all lines, only 35% of claims currently achieve straight-through processing, meaning nearly two-thirds still involve unnecessary human touchpoints [8].

What Changes When You Remove the Manual Layer

The question isn't whether AI can replace adjusters. On complex cases, it can't, and it shouldn't try to. The real question is: which tasks in your claims workflow require human judgment, and which are simply process execution?

For most carriers, the answer is that the majority of manual touchpoints in a standard claims cycle are execution tasks: document validation, policy coverage checks, data entry into case management systems, status communications to claimants, and consistency cross-checks. None of these require underwriting judgment. All of them are being done by people who were hired for their underwriting judgment.

Autonomous AI claims workflows target exactly this layer. The operational results follow directly:

Claims handling time reduced from days to hours, or hours to minutes, for standard cases (demonstrated: 5 days to 30 minutes for travel delay claims).

Manual review touchpoints reduced by up to 80%, with human review reserved for edge cases and complex decisions.

Processing cost falls from $40 to $60 per manual claim to under $20 with automation, a saving that compounds at scale.

Consistency improvements across coverage decisions, fraud flags, and claimant communication.

Scale without proportional cost growth: volume can increase without a corresponding headcount increase.

How to Diagnose the Problem in Your Own Operation

Before investing in any automation, it's worth measuring where manual cost actually sits in your current workflow. Three questions to start with:

What percentage of your adjusters' time is spent on data entry, document retrieval, and system updates, versus actual coverage analysis?

Industry benchmarks suggest 40% is going to admin. If you don't have your own number, that's the first gap.

What is your average handling time for a standard, non-contested claim, and how many human touchpoints does it involve?

The 23.9-day industry average for property claims [1] is a useful benchmark. Where does your operation sit relative to that?

Where are your rework loops?

Track which claims get reopened after initial closure, and why. Five Sigma's analysis shows that claims requiring more than one adjuster take nearly three times as long to resolve. If your rework rate is high, the underlying cost is likely larger than it appears on any single budget line.

The answers will tell you where the cost is, and more importantly, what proportion of it can be systematically removed.

The Bottom Line

Manual claims review isn't a throughput problem. It's a cost structure problem, and one that gets harder to fix the longer it goes unaddressed. Every year of volume growth embeds it deeper into your operating model.

The evidence is consistent across insurance lines. Adjusters spending 40% of their time on admin. Manual claims costing two to three times their automated equivalent. Processing times deteriorating year-on-year. Customer satisfaction tracking directly with speed of resolution. These aren't isolated data points. They're symptoms of the same structural issue.

The carriers moving fastest right now are treating claims automation not as an IT project, but as a financial decision: a structured way to reduce the cost of running their existing portfolio at current volume, while creating the capacity to grow without adding headcount.

That's not a technology bet. It's an operational one.

See it in your own operation

MarvelX AI automates the execution layer of claims processing. Manual review reduced by 80%, no system replacement required, no rebuild of your existing workflow.

Sources

J.D. Power 2024 U.S. Property Claims Satisfaction Study, jdpower.com

J.D. Power 2024 U.S. Auto Claims Satisfaction Study, jdpower.com

Deloitte Insurance Claims Transformation Report, deloitte.com

Five Sigma Labs, Exclusive Data: Claims Adjusters' Day-to-Day Workloads, fivesigmalabs.com

CleverDocs, Manual vs. Automated Claims Processing Cost Analysis, clever-docs.com

Accenture, Poor Claims Experiences Could Put Up to $170B of Global Premiums at Risk by 2027, newsroom.accenture.com

Squaremouth, 2024 Travel Recap: 6 Surprising Travel Industry Trends, squaremouth.com

VariFlight DataWorks, Parametric Insurance & Flight Delay Claims Case Study, June 2025, dataworks.variflight.com

AltexSoft, Parametric Insurance: Travel Insurance & Flight Disruption, altexsoft.com

Number Analytics, Modern Insurance Claims Automation Report, numberanalytics.com

McKinsey, The Future of AI in the Insurance Industry, mckinsey.com

It doesn't show up as a line item. But it's quietly consuming a larger share of your operating budget than almost anything else in your claims operation.

Ask any Head of Claims where their biggest cost sits and you'll hear the same answers: fraud losses, litigation, reinsurance. Manual review rarely makes the list. But strip back the loaded hourly rates, the rework loops, the SLA breach penalties, and the talent cost of keeping experienced adjusters doing repetitive triage, and a different picture emerges.

Manual claims review isn't just slow. It's a structural cost problem that compounds as volume grows, and most insurers are underestimating it by a significant margin. According to J.D. Power's 2024 Property Claims Satisfaction Study, average property claims cycle time has reached 23.9 days, over six days longer than in 2022. For travel insurers, the picture is even sharper: travel insurance claims increased 18% in 2024 compared to 2023 (Squaremouth), meaning that operational debt is growing faster than most operations are equipped to handle.

The Cost You're Not Measuring

Most claims operations measure cost-per-claim as a headline number. What that figure rarely captures is the fully loaded cost of the human steps involved in a manual review cycle. Research from Deloitte's Insurance Claims Transformation Report found that adjusters spend up to 40% of their time on administrative tasks rather than actual claims evaluation. For a function hired to exercise professional judgment, that ratio represents a significant structural inefficiency.

The specific costs that go unmeasured include:

Adjuster time spent on data entry, document retrieval, and coverage cross-referencing. None of these tasks require professional judgment, yet they dominate an adjuster's working day.

Rework cycles triggered by incomplete submissions, incorrect data, or system mismatches, with each loop adding days to handling time.

Escalation overhead when borderline cases get passed up the chain due to lack of a structured decision framework.

SLA breach costs, including both financial penalties and the reputational damage of slow claimant communication.

Opportunity cost: the complex, high-value cases that experienced adjusters never reach because their capacity is absorbed by volume work.

Add these together across a portfolio of thousands of claims per month, and the number stops being a rounding error.

Adjusters spend up to 40% of their time on administrative tasks rather than actual claims evaluation. For a function hired to exercise professional judgment, that ratio is the core of the problem [2].

Volume Is the Multiplier

The problem with manual review isn't just that it's expensive per claim. It's that the cost scales linearly with volume. Every additional claim demands a proportional increase in headcount, tooling, and management overhead, with no efficiency gain at higher throughput.

The data makes this concrete. Manual processing currently costs $40 to $60 per claim compared to under $20 for automated claims. That's a cost differential that becomes unsustainable at scale. For a mid-size carrier processing 10,000 claims per month, even a conservative estimate of 45 minutes of manual handling per claim amounts to roughly 7,500 person-hours monthly. At loaded labour cost, that's a seven-figure annual expense, before a single fraud case is caught or a single SLA breach occurs.

The travel insurance sector illustrates this acutely. With claims volumes up 18% in 2024 and average trip costs rising 25% year-on-year [6], the financial exposure per claim is growing at the same time as volume, compressing margins from both directions. Carriers relying on manual processing to handle this growth are effectively choosing to pay more per claim while handling more of them.

Critically, that cost doesn't decrease when claim complexity decreases. Straightforward, low-value claims consume roughly the same manual touchpoints as complex ones. The effort is in the process, not the case.

Where the Budget Is Actually Going

Across carriers, MGAs, and claims outsourcing providers, the manual review cost structure typically breaks down into three buckets.

1. Direct Labour: the visible cost

Adjuster salaries, team lead oversight, QA review layers, and the management overhead required to maintain throughput. This is the cost most CFOs see on a spreadsheet, but even here, utilisation data is rarely scrutinised. The percentage of adjuster time spent on truly judgment-intensive work is consistently lower than leadership assumes: industry data puts administrative tasks at up to 40% of working time, with the most experienced adjusters most constrained by this.

2. Process Friction: the cost no one owns

Rework loops, missing documentation requests, inconsistent coverage decisions across adjusters, and inter-system data handoffs. These costs are diffuse, never sitting in a single budget line, but compounding across every claim that touches more than one human. Five Sigma's analysis of thousands of real claims found that when a claim requires more than one adjuster, handling time nearly triples (2.75 to 2.85x average)[3]. For a claims operation where multi-adjuster claims are the norm on complex lines, this is not a marginal cost.

3. Downstream Risk: the cost you discover late

SLA penalties, regulatory breach exposure, fraud that slipped through inconsistent review, and claimant churn from poor communication. Accenture's research across 6,700+ policyholders in 25 countries found that poor claims experiences put up to $170 billion in global insurance premiums at risk by 2027 [5]. These costs often appear in different budget lines (legal, compliance, customer retention), making the root cause invisible in reporting.

A Clear Example: Travel Insurance

Travel insurance claims offer one of the sharpest illustrations of what the manual processing cost problem looks like in practice, and what becomes possible when it's removed.

In 2025, an Asia-Pacific travel insurer integrated real-time flight status data into their claims workflow. The result: claim processing time for flight delay claims dropped from five days to under 30 minutes [7]. The same claims. The same coverage. The same adjuster team, now freed from a process that had been consuming their capacity on the most routine, predictable claims in their portfolio.

This isn't an edge case. Travel claims are structurally well-suited to illustrate the broader problem: they involve high volumes of straightforward, verifiable events (delays, cancellations, medical emergencies) that are currently processed through the same manual review channels as complex, high-judgment cases. The overhead is disproportionate to the decision complexity.

Research consistently bears this out. In travel insurance specifically, 60% of claimants cite slow settlement times as a major source of dissatisfaction. Across all lines, only 35% of claims currently achieve straight-through processing, meaning nearly two-thirds still involve unnecessary human touchpoints [8].

What Changes When You Remove the Manual Layer

The question isn't whether AI can replace adjusters. On complex cases, it can't, and it shouldn't try to. The real question is: which tasks in your claims workflow require human judgment, and which are simply process execution?

For most carriers, the answer is that the majority of manual touchpoints in a standard claims cycle are execution tasks: document validation, policy coverage checks, data entry into case management systems, status communications to claimants, and consistency cross-checks. None of these require underwriting judgment. All of them are being done by people who were hired for their underwriting judgment.

Autonomous AI claims workflows target exactly this layer. The operational results follow directly:

Claims handling time reduced from days to hours, or hours to minutes, for standard cases (demonstrated: 5 days to 30 minutes for travel delay claims).

Manual review touchpoints reduced by up to 80%, with human review reserved for edge cases and complex decisions.

Processing cost falls from $40 to $60 per manual claim to under $20 with automation, a saving that compounds at scale.

Consistency improvements across coverage decisions, fraud flags, and claimant communication.

Scale without proportional cost growth: volume can increase without a corresponding headcount increase.

How to Diagnose the Problem in Your Own Operation

Before investing in any automation, it's worth measuring where manual cost actually sits in your current workflow. Three questions to start with:

What percentage of your adjusters' time is spent on data entry, document retrieval, and system updates, versus actual coverage analysis?

Industry benchmarks suggest 40% is going to admin. If you don't have your own number, that's the first gap.

What is your average handling time for a standard, non-contested claim, and how many human touchpoints does it involve?

The 23.9-day industry average for property claims [1] is a useful benchmark. Where does your operation sit relative to that?

Where are your rework loops?

Track which claims get reopened after initial closure, and why. Five Sigma's analysis shows that claims requiring more than one adjuster take nearly three times as long to resolve. If your rework rate is high, the underlying cost is likely larger than it appears on any single budget line.

The answers will tell you where the cost is, and more importantly, what proportion of it can be systematically removed.

The Bottom Line

Manual claims review isn't a throughput problem. It's a cost structure problem, and one that gets harder to fix the longer it goes unaddressed. Every year of volume growth embeds it deeper into your operating model.

The evidence is consistent across insurance lines. Adjusters spending 40% of their time on admin. Manual claims costing two to three times their automated equivalent. Processing times deteriorating year-on-year. Customer satisfaction tracking directly with speed of resolution. These aren't isolated data points. They're symptoms of the same structural issue.

The carriers moving fastest right now are treating claims automation not as an IT project, but as a financial decision: a structured way to reduce the cost of running their existing portfolio at current volume, while creating the capacity to grow without adding headcount.

That's not a technology bet. It's an operational one.

See it in your own operation

MarvelX AI automates the execution layer of claims processing. Manual review reduced by 80%, no system replacement required, no rebuild of your existing workflow.

Sources

J.D. Power 2024 U.S. Property Claims Satisfaction Study, jdpower.com

J.D. Power 2024 U.S. Auto Claims Satisfaction Study, jdpower.com

Deloitte Insurance Claims Transformation Report, deloitte.com

Five Sigma Labs, Exclusive Data: Claims Adjusters' Day-to-Day Workloads, fivesigmalabs.com

CleverDocs, Manual vs. Automated Claims Processing Cost Analysis, clever-docs.com

Accenture, Poor Claims Experiences Could Put Up to $170B of Global Premiums at Risk by 2027, newsroom.accenture.com

Squaremouth, 2024 Travel Recap: 6 Surprising Travel Industry Trends, squaremouth.com

VariFlight DataWorks, Parametric Insurance & Flight Delay Claims Case Study, June 2025, dataworks.variflight.com

AltexSoft, Parametric Insurance: Travel Insurance & Flight Disruption, altexsoft.com

Number Analytics, Modern Insurance Claims Automation Report, numberanalytics.com

McKinsey, The Future of AI in the Insurance Industry, mckinsey.com