MarvelX Team

MarvelX Team

·

FNOL automation: turning first notice of loss into a started claim in seconds

FNOL automation: turning first notice of loss into a started claim in seconds

The FNOL bottleneck is intake, not adjudication

Most motor claims do not stall at the decision. They stall at the start. A handler reads the FNOL, transcribes the details into the claims system, and validates the policy by hand. Each step is slow, each step invites re-keying errors, and every volume spike stretches the intake queue from hours into days.

The claimant waits without an acknowledgement while handlers do data entry instead of judgment calls. For a mid-size motor insurer, this intake lag is a fixed tax on every claim. It caps how many claims a team can start in a day and ties headcount to volume. The problem is not that adjudication is hard. The problem is that the claim takes too long to become a claim at all.

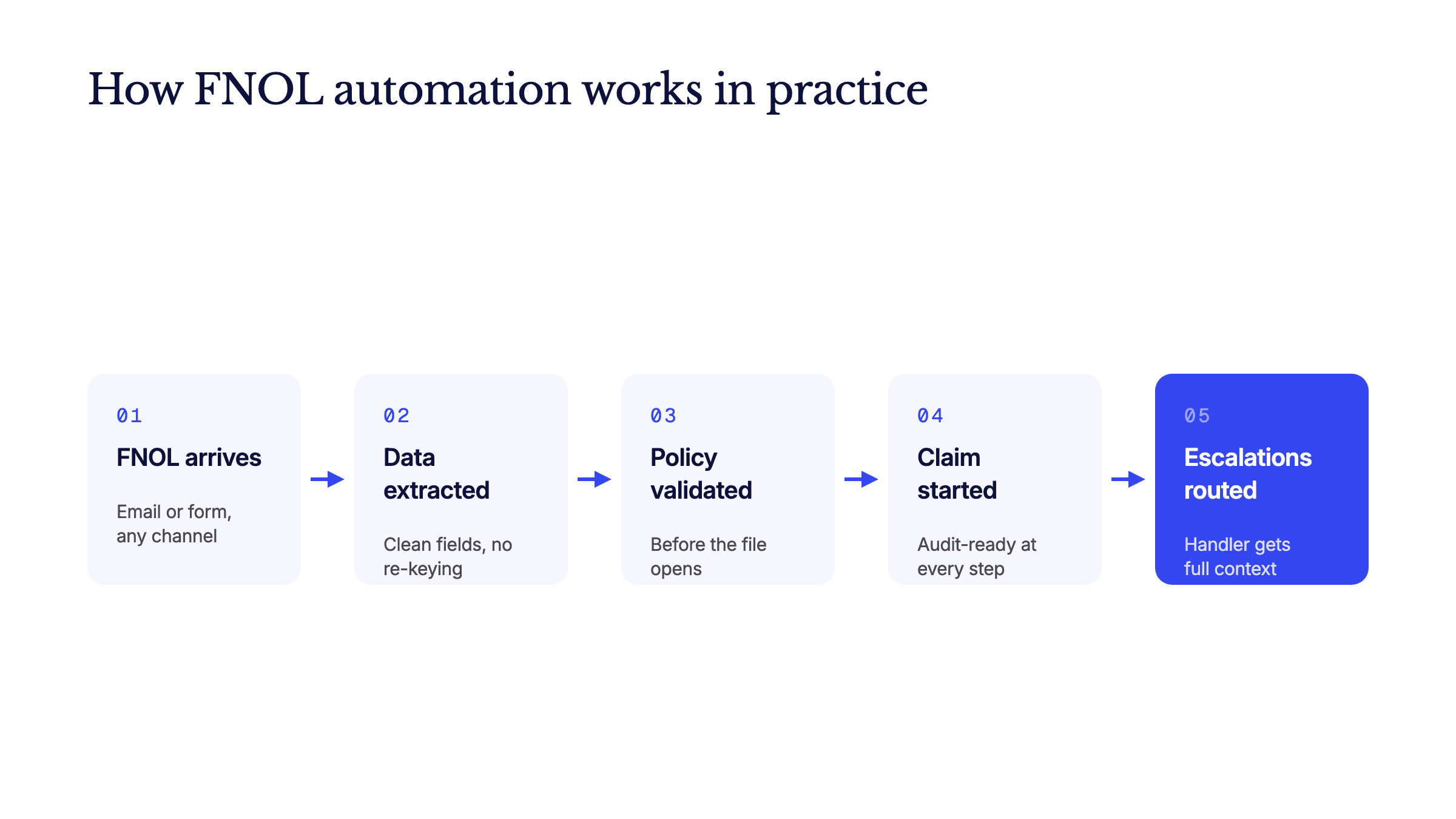

How FNOL automation works in practice

The AI claims agent starts the moment the FNOL arrives. It ingests the notification, extracts the structured data, and runs policy validation to open the claim with no re-keying. The details land in your claims system as clean, structured fields. Every step produces audit-ready output, so you can trace exactly what the agent read and what it did.

Human oversight stays central by design. When a claim falls below the confidence threshold, it routes to a handler with full context, not a blank form. The handler sees the extracted data, the validation result, and the reason for escalation. Handlers spend their time on the judgment calls that genuinely need human review.

When the FNOL is incomplete

The first question most claims leaders ask is what happens when the FNOL is not clean. In production, the agent checks completeness at intake. When documents are missing or the policy cannot be identified, it asks the claimant for exactly the missing items at the moment of notification. The gap closes on day one, instead of a handler discovering it days later and restarting the exchange.

What changes for your team

Faster intake changes what your team does all day: handlers stop transcribing and start deciding. In an embedded insurance case study, claim processing time fell from days to under an hour. The same client reached 10x claims capacity without a headcount increase, so volume spikes no longer force hiring.

One distinction keeps those numbers honest. Intake takes seconds: the claim exists and is acknowledged the moment the FNOL lands. Under an hour covers the full processing of the claim that follows.

Independent research points the same way. McKinsey reports that Aviva rolled out more than 80 AI models and cut liability assessment time for complex cases by 23 days. McKinsey also projects that many claims will be resolved in minutes rather than days or weeks by 2030. Oversight does not shrink in this model: handlers review escalations with full context, and audit-ready output documents every step for regulators.

Key takeaway

FNOL automation removes the manual intake lag that stalls claims before adjudication begins, and it keeps human oversight on every decision that needs judgment.

Frequently asked questions

What does FNOL automation actually do?

An AI claims agent ingests the First Notice of Loss (FNOL), extracts the structured data, and runs policy validation to open the claim with no re-keying. It moves the claim into your system as clean, structured fields. This removes the manual intake step that adds days to cycle time.

Does FNOL automation remove the human handler?

No. The agent handles the mechanical intake that should not require human judgment, and handlers keep oversight on the decisions that do. Claims below the confidence threshold route to a handler with full context, not a blank form.

What results have insurers seen from automating claims intake?

In an embedded insurance case study, claim processing time fell from days to under an hour, and that client reached 10x claims capacity without a headcount increase. Separately, McKinsey reports Aviva cut liability assessment time for complex cases by 23 days using more than 80 AI models.

Further reading

Request A Demo

The FNOL bottleneck is intake, not adjudication

Most motor claims do not stall at the decision. They stall at the start. A handler reads the FNOL, transcribes the details into the claims system, and validates the policy by hand. Each step is slow, each step invites re-keying errors, and every volume spike stretches the intake queue from hours into days.

The claimant waits without an acknowledgement while handlers do data entry instead of judgment calls. For a mid-size motor insurer, this intake lag is a fixed tax on every claim. It caps how many claims a team can start in a day and ties headcount to volume. The problem is not that adjudication is hard. The problem is that the claim takes too long to become a claim at all.

How FNOL automation works in practice

The AI claims agent starts the moment the FNOL arrives. It ingests the notification, extracts the structured data, and runs policy validation to open the claim with no re-keying. The details land in your claims system as clean, structured fields. Every step produces audit-ready output, so you can trace exactly what the agent read and what it did.

Human oversight stays central by design. When a claim falls below the confidence threshold, it routes to a handler with full context, not a blank form. The handler sees the extracted data, the validation result, and the reason for escalation. Handlers spend their time on the judgment calls that genuinely need human review.

When the FNOL is incomplete

The first question most claims leaders ask is what happens when the FNOL is not clean. In production, the agent checks completeness at intake. When documents are missing or the policy cannot be identified, it asks the claimant for exactly the missing items at the moment of notification. The gap closes on day one, instead of a handler discovering it days later and restarting the exchange.

What changes for your team

Faster intake changes what your team does all day: handlers stop transcribing and start deciding. In an embedded insurance case study, claim processing time fell from days to under an hour. The same client reached 10x claims capacity without a headcount increase, so volume spikes no longer force hiring.

One distinction keeps those numbers honest. Intake takes seconds: the claim exists and is acknowledged the moment the FNOL lands. Under an hour covers the full processing of the claim that follows.

Independent research points the same way. McKinsey reports that Aviva rolled out more than 80 AI models and cut liability assessment time for complex cases by 23 days. McKinsey also projects that many claims will be resolved in minutes rather than days or weeks by 2030. Oversight does not shrink in this model: handlers review escalations with full context, and audit-ready output documents every step for regulators.

Key takeaway

FNOL automation removes the manual intake lag that stalls claims before adjudication begins, and it keeps human oversight on every decision that needs judgment.

Frequently asked questions

What does FNOL automation actually do?

An AI claims agent ingests the First Notice of Loss (FNOL), extracts the structured data, and runs policy validation to open the claim with no re-keying. It moves the claim into your system as clean, structured fields. This removes the manual intake step that adds days to cycle time.

Does FNOL automation remove the human handler?

No. The agent handles the mechanical intake that should not require human judgment, and handlers keep oversight on the decisions that do. Claims below the confidence threshold route to a handler with full context, not a blank form.

What results have insurers seen from automating claims intake?

In an embedded insurance case study, claim processing time fell from days to under an hour, and that client reached 10x claims capacity without a headcount increase. Separately, McKinsey reports Aviva cut liability assessment time for complex cases by 23 days using more than 80 AI models.